How to Become a Mortgage Loan Officer in Washington: Requirements and Hours

Evergreen State housing never slows down. Neither should you.

Licensed originators are in demand across Washington, and the path starts with 22 hours that you can finish online. Get started on your schedule.

Quick Answer:

- The short version: register with the NMLS, complete 22 hours of approved education, pass the SAFE exam, apply through the Washington DFI, clear a background and credit check, then get sponsored.

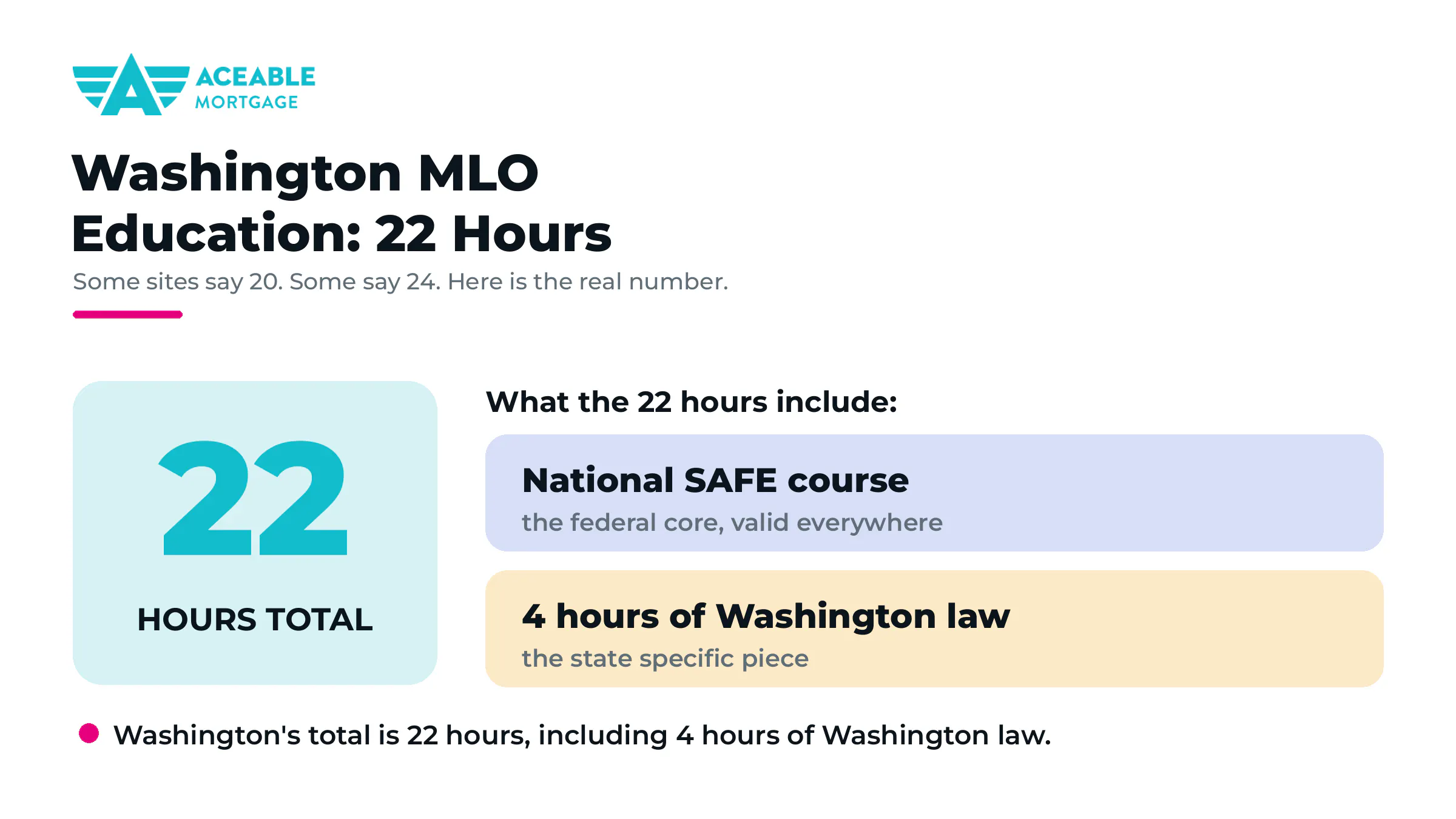

- The hours: Washington requires 22 hours of pre licensing education, which is the 20 hour national SAFE course plus 4 hours of Washington law, with overlap that brings the posted total to 22.

- The catch most people miss: pre licensing education and continuing education are not interchangeable, so take the pre licensing version.

If you are searching for how to become a mortgage loan officer in Washington, here is the direct answer: you complete six steps, anchored by 22 hours of education and the national SAFE exam, then get sponsored by an employer.

How do you become a mortgage loan officer in Washington?

You become a licensed mortgage loan originator in Washington by completing these six steps in order. The Washington State Department of Financial Institutions, known as the DFI, is the regulator that issues the license.

- Register with the NMLS. Create your account to get your unique NMLS ID, which stays with you throughout your career and across all states.

- Complete 22 hours of pre-licensing education. Take the 20-hour national SAFE course plus 4 hours of Washington law through an NMLS-approved provider, and be sure it is pre-licensing, not continuing education.

- Pass the SAFE MLO national exam. Score at least 75 percent on the national test, scheduled once your education posts.

- Apply through the Washington DFI. File your license application in the NMLS for review by the Department of Financial Institutions.

- Clear the background and credit checks. Complete fingerprinting, a criminal background check, and a credit report authorization.

- Get sponsored. Have a state-licensed employer sponsor your NMLS ID to originate loans in Washington.

The order is not optional. You cannot submit your application until your education and exam results are posted to your NMLS record, and your license will not activate until an employer sponsors your NMLS ID.

What does a mortgage loan originator do?

A mortgage loan originator, or MLO, takes residential mortgage loan applications and offers or negotiates home loan terms for compensation. You are the licensed guide who moves a borrower from application to approval, matching them to loan products and steering the paperwork. It is a commission-driven career with real upside, which is why so many career changers find their way to it.

MLO, loan officer, or mortgage broker: what is the difference?

The titles blur together, but they are not the same. A loan officer and a mortgage loan originator are essentially the same licensed role, taking applications for an employer. A mortgage broker runs an independent business that connects borrowers with multiple lenders and may supervise originators. All three require NMLS licensing, but the broker adds a business layer on top. If you are deciding which path fits, our breakdown of these three rolesPre License Mlo Vs Loan Officer Vs Mortgage Broker Resources sorts out the differences.

Washington education requirement: 22 hours

Washington requires 22 hours of NMLS-approved pre-licensing education, including 4 hours of Washington law. This is higher than the 20-hour federal SAFE floor, and the way the total lands at 22 is worth explaining clearly, because competitor pages often get it wrong.

The foundation is the 20-hour national SAFE course, standardized everywhere: 3 hours of federal law, 3 hours of ethics covering fraud, consumer protection, and fair lending, 2 hours of nontraditional mortgage products, and 12 hours of electives. Washington then requires 4 hours of Washington-specific law.

Because of how the state structures the overlap between the national curriculum and its own requirement, the posted total comes to 22 hours rather than a straight 24.

The practical takeaway is simple: enroll in a course package that posts 22 Washington hours to your NMLS record. Knowing this structure is the foundation of any honest look at getting licensedPre License How To Become A Mortgage Loan Originator Resources as an originator.

Is pre-licensing the same as continuing education?

No, and this is the mistake that quietly derails applications. Washington requires pre-licensing education specifically. Continuing education courses, the kind licensed originators take each year to renew, do not satisfy the pre-licensing requirement, even when the subject matter overlaps. When you enroll, confirm the course is labeled pre-licensing education, not continuing education. The same care applies later when you maintain the license through annual renewalPre License Mlo Continuing Education Resources.

How do you pass the SAFE MLO national exam?

Once your education posts are complete, you sit the SAFE MLO national test through your NMLS account. The exam has 120 questions, of which 115 are scored, and you need at least 75 percent to pass. The national first-time pass rate runs below 60 percent, so preparation is not optional.

That sub-60 percent pass rate tells you the test is genuinely demanding. The federal law and ethics content sinks the most candidates, and the exam rewards understanding over rote recall. A study plan built around the test content outline beats simply re-reading the course, which is why focused exam preparationPre License Nmls Exam Prep Resources pays for itself on the first attempt.

What happens if I fail the exam?

You can retake it, with waiting periods that lengthen as failures accumulate. You wait 30 days between each of your first three attempts. After a third consecutive failure, the wait extends to 180 days before you can test again, and each attempt needs a separate enrollment. The structure is built to encourage serious preparation rather than repeated attempts, so make your first try the one that counts.

Choose a State and Course

What is the income ceiling for a Washington MLO?

Commission earning has no cap, and Washington's housing market gives originators room to run. See the earnings breakdown.

How do you apply for your Washington license through the DFI?

With education and exam behind you, you file through the NMLS, and the Washington State Department of Financial Institutions reviews the application. It includes a criminal background check with fingerprinting and authorization for a credit report. Applicants not already licensed in another state schedule fingerprinting promptly after applying. Like every state, Washington weighs financial responsibility, so unresolved credit issues can prompt additional review.

Can I take my courses online?

Yes. NMLS approved providers offer the 22 hours in a range of formats, including fully online instructor led courses and classroom options, so you can complete the requirement on your own schedule. The only firm rule is that the provider must be NMLS approved and the course must be the pre licensing version. For a broader picture of how the national system fits together, our overview of the NMLS is a useful primer.

How do you get employer sponsorship?

This is the step that catches first timers off guard. Passing the exam and getting your application approved does not produce an active license on its own. In Washington, you can hold an approved but inactive license without a sponsor, but you cannot actually originate loans until a state licensed employer sponsors your NMLS ID.

Most candidates line up a sponsoring employer during the licensing process so sponsorship can be approved soon after the license is. If you are interviewing while you study, treat sponsorship as part of your timeline, because the career does not begin until it is in place.

What can slow down your Washington MLO license?

- Taking the wrong course type. Continuing education does not satisfy the pre licensing requirement, and mixing them up means redoing hours.

- The 22 hour confusion. Enroll in a package that posts the full 22 Washington hours, not just the bare 20 national hours.

- Credit and background issues. Unresolved judgments or a thin explanation of past financial trouble can trigger additional DFI review.

- Failing the exam. A third failure means a 180 day wait, which can delay your start by half a year.

- No sponsor. Without a sponsoring employer, your license stays inactive and you cannot originate.

How long does it take to become an MLO in Washington?

Most candidates move from first course enrollment to an issued license in roughly two to four months, with the pace largely under your control. The 22 hours of education can be done in one to two weeks of focused study, the exam is scheduled once your hours post, and DFI review of a complete application generally takes a couple of weeks. The timeline stretches with exam retakes, credit or background items needing explanation, and how quickly sponsorship is arranged. Candidates who secure an employer early and prepare thoroughly for the exam tend to finish faster.

How does Washington compare to other states?

Washington's 22 hour requirement sits just above the 20 hour federal minimum, making it one of the lighter state add ons in the country. States that tack on a full 4 hour law course without overlap land at 24, while a handful require only the bare 20. The national SAFE exam and the sponsorship rule are identical everywhere, since both flow from federal law, so the Washington law hours and the precise 22 hour total are really the only state specific wrinkles. For a sense of where the career leads once you are licensed, our look at originator earning potential sets realistic expectations.

How to become a mortgage loan officer in Washington: FAQ

How do I become a mortgage loan officer in Washington?

Register with the NMLS, complete 22 hours of approved pre licensing education, pass the SAFE national exam, apply through the Washington DFI, clear a background and credit check, and get employer sponsorship.

How many education hours does Washington require?

Twenty two hours, which is the 20 hour national SAFE course plus 4 hours of Washington law, with overlap that brings the posted total to 22. This is more than the 20 hour federal minimum.

Who regulates mortgage loan originators in Washington?

The Washington State Department of Financial Institutions, with applications processed through the NMLS.

Is the pre licensing course the same as continuing education?

No. Washington requires pre licensing education specifically, and continuing education courses do not satisfy the pre licensing requirement.

How hard is the SAFE exam?

The national pass rate is below 60 percent, so candidates are strongly encouraged to use exam preparation before testing.

Start your Washington MLO career

Becoming a mortgage loan officer in Washington comes down to a clear sequence: register, complete your 22 hours, pass the SAFE exam, apply through the DFI, and get sponsored. The 22 hour total and the pre licensing versus continuing education distinction are the two pieces worth getting right from the start. Aceable Mortgage is building a modern, mobile first pre licensing experience designed to get Washington originators exam ready without the dry textbook slog. Get your Washington MLO education started by joining the waitlist for notification at launch.

Last reviewed by the Aceable Mortgage compliance content team against Washington State Department of Financial Institutions and NMLS pre licensing requirements.

Sources: Washington State Department of Financial Institutions and the NMLS Resource Center.

Your Washington MLO license starts here.

The 20-hour SAFE course plus 4 hours of Washington law, the real 22, done on your phone and built to help you pass. Start when you are ready.